UPDATE! If you're looking for a more recent review of Samaritan (I wrote this when we'd been members just a few months), click here:

Or here:

https://lissa-anglin.squarespace.com/blog/2013/4/16/samaritan-ministries-review-a-year-later

A while back I mentioned that we'd selected a bit of a non-traditional approach to healthcare coverage- selecting Samaritan Ministries over the typical medical insurance we'd had for the past 5 years.

Now that we're several months in, I thought it might be nice for me to update you all (yes- all 2 of you who might be interested- haha) on how things are going.

If you just jumped in on this conversation, Samaritan Ministries is a faith-based non-insurance approach to healthcare. Its basis is firmly grounded on the concept of believers sharing the needs and burdens of other believers. Instead of paying in to an insurance company, my monthly "share" is sent directly to another member who is needing it to cover medical costs. Each members' share is determined by the number of people in their household.

So far, it's been the right decision for our family- especially since we are both self-employed now, me with my photography business, and Shawn with Culture Clothing.

Being a Pros/Cons type of thinker, I'm going to write out a list for your reading pleasure (and also a bit for my personal reflection).

Cons:

1. The monthly "share" (a.k.a. payment) is more expensive than what we'd been paying (320.00 as opposed to 240.00). As a family of three, we pay the highest amount of any category (The others are singles and couples- and they also have a special rate for those attending college). The sunny side of this is that because we pay the highest rate already, our rate will never increase because of more children. Knowing this has granted us a sense of peace, instead of fear for increased costs as we grow our family.

2. Doesn't cover pre-existing conditions. This is typical with many insurance plans, but it is tough for members that have chronic problems. Thankfully, we have not had to deal with any of this sort.

3. No Dental coverage. While we used to have additional coverage for dental, it is not covered with Samaritan. We are hoping to find regular insurance for this soon.

Pros:

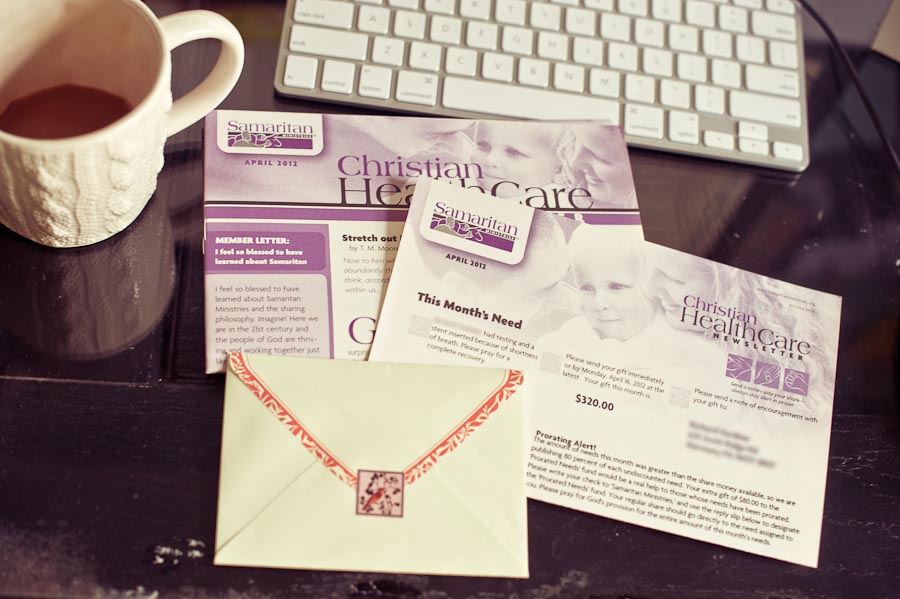

1. I love getting my "newsletter" (a.k.a. bill) in the mail. WHAT? ARE YOU SERIOUS? Yes, I am serious. The newsletter they send with the name and address of the person I will be sending our share to is packed with relevant articles and updates on the ministry. I love that I can understand how it all works (something that I NEVER experienced with our previous insurance) and that the board of directors is constantly updating me on the financial state of the ministry and how I can be in prayer for it.

One of the best parts of the newsletter is reading the "New Rewards" section, which celebrates each new baby that was born to members that month. The "Final Rewards" section is also a blessing to read- documenting each life that has passed- including miscarriages.

2. I get to write a check to A PERSON. Each newsletter I get lets me know the specific person (and address) to send my monthly share to, along with the medical condition it applies to. They encourage members to "Send a note, pay your share, always stay alert in prayer". Though we haven't had a need to be met yet, I know that when we are in that position it will be such a blessing to receive encouraging words from other believers. Note: The first 2 months of our membership we actually sent our share to Samaritan Ministries itself- this covers administrative costs and also establishes us as faithful members.

3. Babies. Samaritan's Maternity coverage is outstanding. After reading their guidelines on Maternity Coverage, I even thought about doing a home birth, since they can be covered up to 100%. We'll see if that actually comes to fruition, though- my husband is having serious doubts about whether or not I can actually take the pain. :) Home birth or not, though- the coverage is great.

4. Deductible. Samaritan essentially has a $300 deductible on any need. This means that any well check for Knox or clinic visit for us will cost us cash out-of-pocket. This is not a big deal since we have structured our household financially to be able to cash-flow these items. Initially we thought we'd need to create a small savings account just for these needs, but so far we have just been paying costs as we go.

Why is this in the Pro section? Because this $300 amount is lower than many of the "deductibles" we've had in the past, AND because in many situations it can be reduced if not erased completely. Because we are technically "uninsured", we pay a different amount at the doctors' offices- most of the time, less than we did when running everything through our insurance. And, since we are "uninsured", if we are able to work out any discounts with the medical provider, they can be applied to our $300. So, if we are able to work out a discount of or over $300, our "deductible" goes to $0.

5. Spiritual coverage. Never before have I been so encouraged to take every need to Jesus. The evidence of His provisions for us in this area of our lives alone has been one of the most faith-strengthening experiences for me, ever. I love knowing that I get to bear another member's burden, and that when I am in need, others will be there to help me and pray for me. It's so simple- and exactly what God has called us to do.

There are many straight-forward answers to the how-does-it-work and what-if questions on their FAQ page HERE.

All in all, we have been blessed to be a part of this ministry. I hope this was helpful for some of you! I'd love to hear your thoughts on this- please feel free to start a convo in the comments!